The catch-up Concessional Contribution rules allow individuals with superannuation balances of less than $500,000 at the end of the previous financial year (30 June 2023), the ability to access their unused concessional contributions cap to make additional concessional (before-tax) contributions. Individuals are able to access their unused concessional contributions on a rolling basis for a period of 5 years. Amounts carried forward that have not been used after 5 years will expire. Only unused amounts accrued from 1 July 2018 can be carried forward.

Let’s explore the case study of Sarah, who strategically leverages catch-up contributions to build up her financial future and save tax.

Background

Sarah who works full time as a manager earning $90,000 annually, has maintained a stable income over the past five years. Her employer has consistently made compulsory contributions to Sarah’s superannuation fund on her behalf. Sarah has not made any additional concessional contributions during this time. Her total employer contributions over the last five financial years and including this year amount to approximately $55,000. As of now, Sarah’s superannuation balance stands at $300,000, with a balance of approximately $270,000 as of 30 June 2023.

Financial Circumstances

Recently, Sarah sold an investment property, anticipating a taxable capital gain of $120,000. Sarah seeks advice from a Financial Planner and Accountant.

Catch-Up Contribution Strategy

Upon consultation with her Financial Planner and Accountant, Sarah decides to capitalise on the catch-up concessional contribution scheme. The Financial Planner recommends that Sarah make a catch-up concessional contribution of $100,000 into her superannuation account and subsequently claim a tax deduction for this contribution. This is the amount she had available to carry forward from the last 5 financial years including the current financial year. Sarah ensures that she lodges a valid Notice of Intent Form within the required timeframe and receives acknowledgement by her super fund.

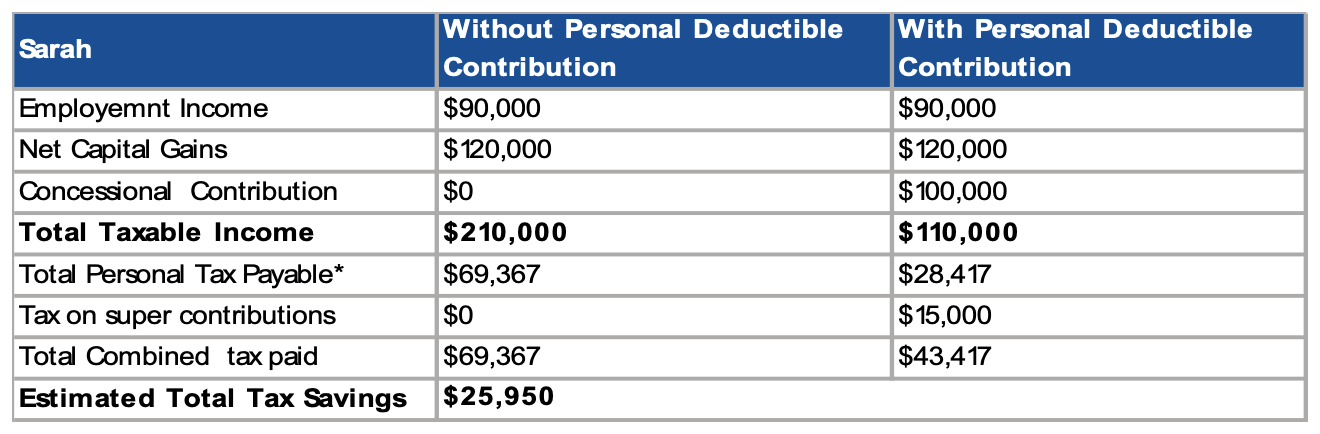

The following table can help to demonstrate this.

*Based on personal income tax rates for 2023/24 income year, including Medicare levy.

Benefits and Results

By implementing the catch-up contribution strategy, Sarah anticipates significant tax savings. Claiming a tax deduction for the $100,000 catch-up contribution is projected to save her approximately $26,000 in tax. This proactive approach not only improves Sarah’s tax position but also substantially bolsters her retirement savings, setting her on a path towards more comfortable retirement.

Conclusion

Sarah’s case exemplifies the strategic use of catch-up concessional contributions to enhance retirement savings and access tax concessions. By proactively engaging with her Financial Planner and leveraging available strategies like the catch-up contributions, Sarah empowers herself to achieve her long-term financial goals with confidence and clarity. You can use MyGov to check your total superannuation balance on previous 30 June and to find out the amount of unused concessional contributions cap that is available to you.

To find out whether you could benefit from this strategy, you should speak to a Financial Planner and a registered tax agent.

Making Personal Deductible Contributions or Salary Sacrifice Contributions to super can be a tax-effective strategy to increase superannuation funds and save you money on tax. Concessional contributions are taxed within superannuation at a rate of up to 15%. If you are a high-income earner, additional tax of 15% may also be applied to concessional contributions.

Investment earnings are taxed at up to 15% within superannuation.

However, amounts contributed to superannuation will be preserved until certain requirements are met.